Valuation After New UK Defence Hub And ESA Quantum Satellite Contract")

Redwire (RDW) is on investor radar after two fresh European developments: a new United Kingdom office focused on UK Ministry of Defence programs and a contract to build a quantum secure satellite for the European Space Agency.

See our latest analysis for Redwire.

These European contracts and the new UK defence hub come as Redwire’s share price sits at $9.29, with a 90 day share price return of a 15.39% decline but a very large 3 year total shareholder return that suggests long term holders have already seen a strong move.

If you are interested in other space and defence names linked to quantum secure communications and advanced payloads, this is a good moment to scan 24 quantum computing stocks

So with Redwire trading at $9.29, sitting on a 90 day share price return decline of 15.39% but a very large 3 year total shareholder return, are you looking at a reset entry point or a market that is already pricing in future growth?

Most Popular Narrative: 30% Undervalued

At $9.29, the most followed narrative pegs Redwire’s fair value at $13.28, applying a specific growth and margin path that differs from the recent 90 day share price weakness.

The rapid proliferation of commercial satellites and upcoming public/private low Earth orbit projects continues to build demand for Redwire’s advanced in-space manufacturing, deployable structures, and subsystems, supporting multi-year visibility on high-margin product sales and recurring earnings.

Curious what earnings profile and revenue ramp this narrative is baking in to reach that fair value and future multiple assumptions? The full narrative spells out the growth mix, margin shift and time horizon behind that $13.28 figure and shows how they tie those projections back using a 7.77% discount rate and a richer future earnings multiple than many peers.

Result: Fair Value of $13.28 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this narrative can break quickly if the timing of government contracts remains unpredictable or large fixed price projects encounter cost overruns and margin pressure.

Find out about the key risks to this Redwire narrative.

Another View On Valuation

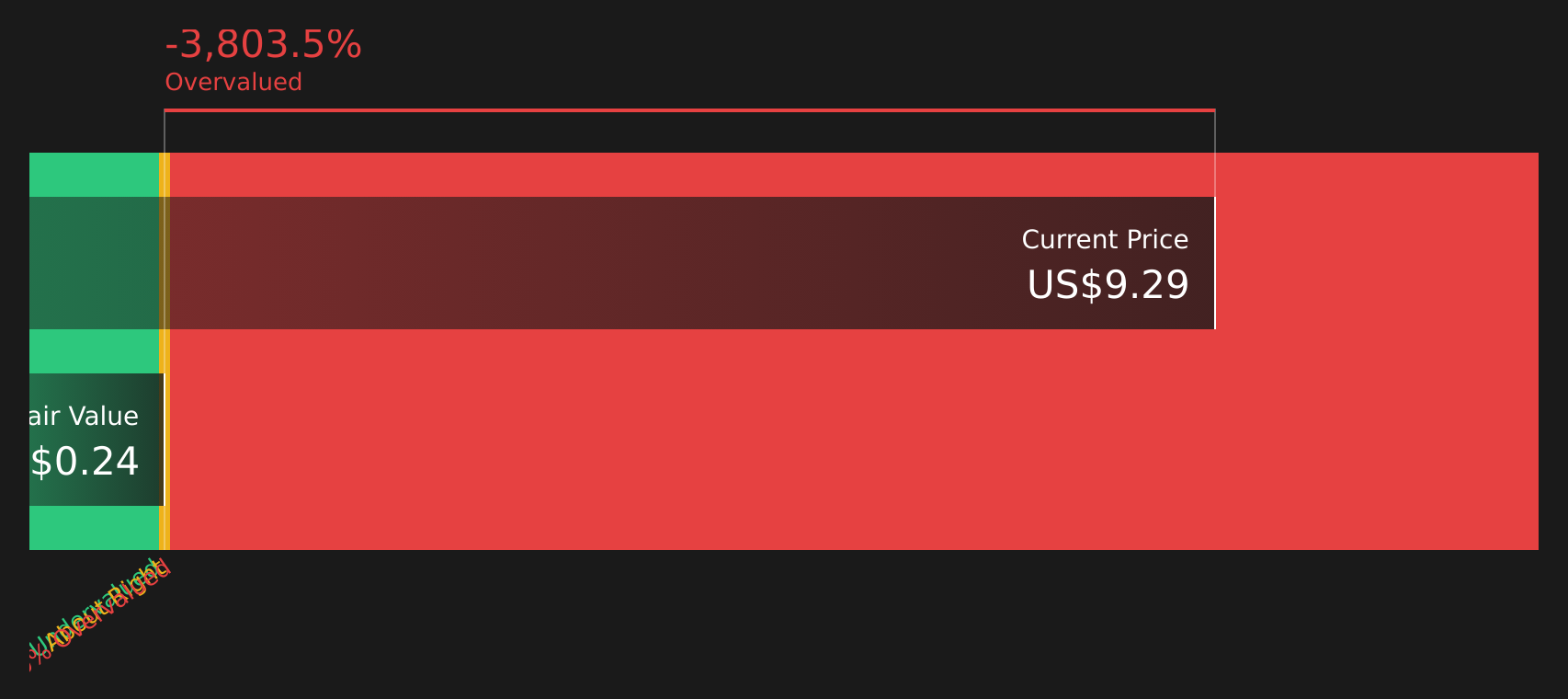

The most popular fair value story says Redwire looks about 30% undervalued at $9.29 versus $13.28. However, the SWS DCF model tells a different story, with an estimate of $0.24 per share that implies the stock is trading far above its modeled future cash flows. Which lens do you trust more?

Look into how the SWS DCF model arrives at its fair value.

RDW Discounted Cash Flow as at Apr 2026Next Steps

RDW Discounted Cash Flow as at Apr 2026Next Steps

With such a split view between fair value models, it makes sense to check the underlying data yourself and decide quickly where you stand, including weighing up the 1 key reward and 4 important warning signs

Looking for more investment ideas?

Redwire might sit at the center of your research today, but you give yourself a real edge when you line it up against other targeted opportunities on the Screener.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com