Is Up 18.0% After ESA’s First Celeste Navigation Launch Success – Has The Bull Case Changed?")

On 28 March 2026, the European Space Agency announced that Rocket Lab’s Electron rocket successfully launched the “Daughter Of The Stars” mission from New Zealand, placing ESA’s first two “Celeste” low Earth orbit navigation demonstration satellites into a 510 km orbit. This mission, which maintained Rocket Lab’s 100% success record for national space programs and marked its 6th launch of 2026 and 85th overall, underscores the company’s growing role as a reliable commercial provider for government and agency missions across navigation, security, and advanced communications. We’ll now explore how this successful ESA mission, alongside Rocket Lab’s broader government work, might influence its investment narrative and risk profile.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Rocket Lab Investment Narrative Recap

To own Rocket Lab, you need to believe its move from “just a launcher” to an end to end space infrastructure provider can offset heavy Neutron spending and ongoing losses. The ESA success reinforces Electron’s reliability and strengthens the case for more agency work, but it does not fundamentally change the near term cash burn and dilution risk that remain central to the story.

The most relevant recent development alongside the ESA launch is Rocket Lab’s progress toward acquiring Mynaric, a specialist in laser communications. While the ESA mission showcases Electron’s role for European agencies, Mynaric would deepen Rocket Lab’s European footprint and expand its space systems offering, tying directly into the core catalyst of winning larger, stickier government and constellation contracts on both sides of the Atlantic.

Yet while the ESA win grabs headlines, investors should also be aware that the real pressure point may be Rocket Lab’s continued high cash consumption and potential dilution risk…

Read the full narrative on Rocket Lab (it’s free!)

Rocket Lab’s narrative projects $1.3 billion revenue and $113.4 million earnings by 2028.

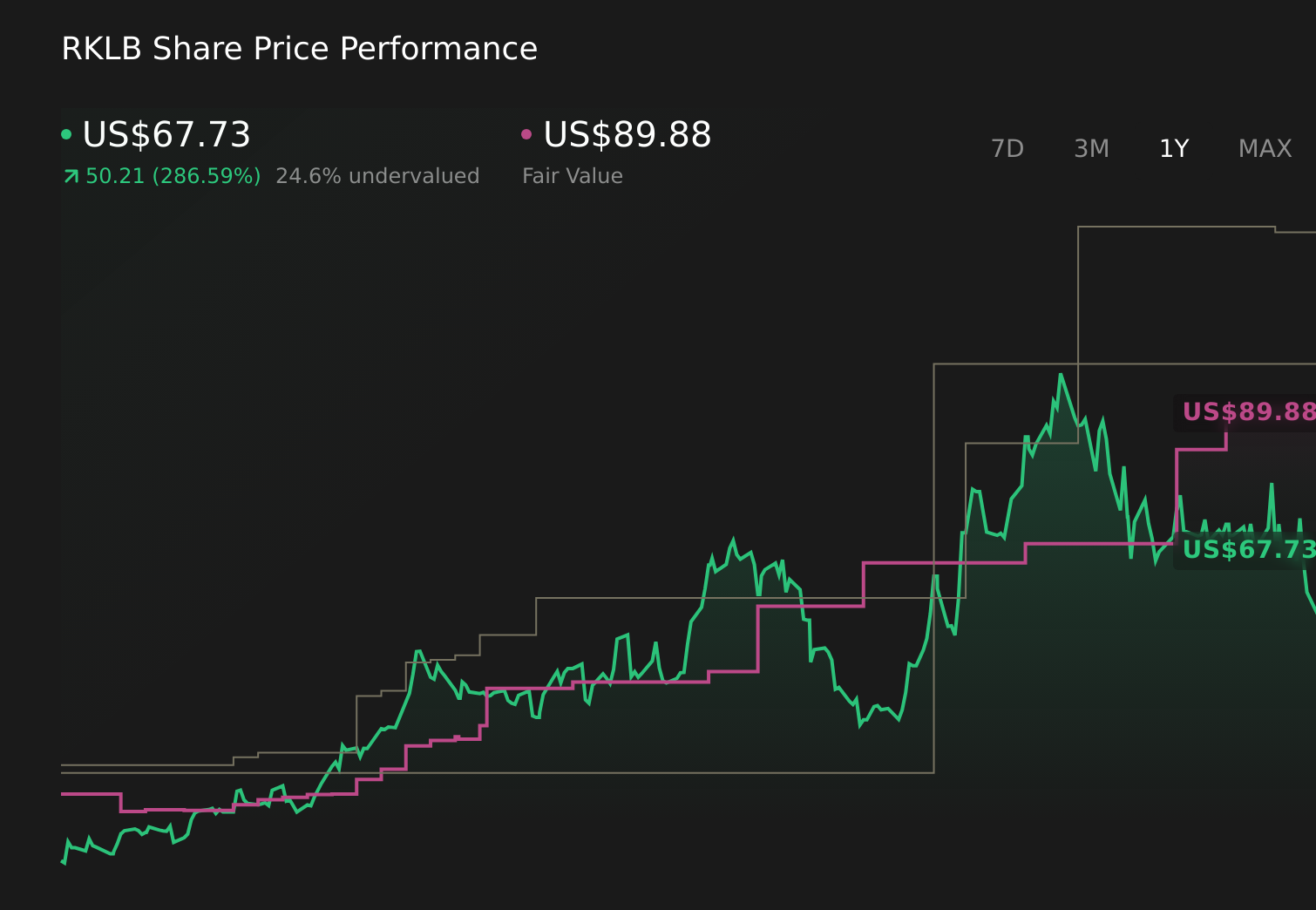

Uncover how Rocket Lab’s forecasts yield a $89.88 fair value, a 33% upside to its current price.

Exploring Other Perspectives RKLB 1-Year Stock Price Chart

RKLB 1-Year Stock Price Chart

While consensus focuses on steady growth and funding risk, the most optimistic analysts see ESA style wins feeding a far bigger story, with revenue possibly reaching US$2.0 billion and earnings US$300.0 million by 2029, so it is worth weighing how this new mission might shift such bullish expectations against your own view of Rocket Lab’s trajectory.

Explore 54 other fair value estimates on Rocket Lab – why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Ready To Venture Into Other Investment Styles?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com